Business

Trading volumes drop to 20-month low at PSX

- Political unrest, rupee depreciation add to woes of local investors.

- KSE-100 index sheds 286.44 points to settle at 43,366.89.

- Shares of 334 companies were traded during the session.

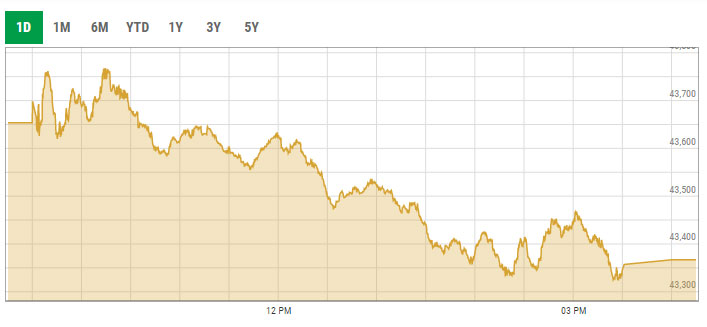

KARACHI: Trading volumes at the Pakistan Stock Exchange (PSX) dropped to a 20-month low on Monday with 115 million shares changing hands during the trading session.

Overall trading volumes declined to 115.11 million shares compared with Friday’s tally of 149.29 million. The value of shares traded during the day was Rs3.64 billion.

The lacklustre performance at the bourse was witnessed due to rising political unrest in the country in the wake of a no-confidence motion against Prime Minister Imran Khan.

Moreover, the depreciation of the Pakistani rupee against the US dollar — which dropped to an all-time low of Rs178.98 — coupled with rising commodity prices in the international market added fuel to the downtrend.

Investor interest was mostly witnessed in the fertiliser sector over increasing urea prices where Engro Fertiliser, Fauji Fertiliser and Fauji Fertiliser Bin Qasim closed on a higher note

At the close, the benchmark KSE-100 index shed 286.44 points, or 0.66%, to settle at 43,366.89 points.

Arif Habib Limited in its post-market commentary noted that a range-bound session was observed today due to political unrest.

“The market opened in the green zone and stayed volatile throughout the day,” it said, adding that mainboard activity remained dull.

On the flip-side, activity continued to remain side-ways as the market witnessed hefty volumes in the third-tier stocks. The brokerage house stated that in the last trading hour, across the board selling was witnessed which led the index to close in the red zone.

Sectors contributing to the performance included exploration and production (-57.7 points), banks (-56.7 points), cement (-56.5 points), technology (-52.2 points) and power (-29 points).

Shares of 334 companies were traded during the session. At the close of trading, 79 scrips closed in the green, 242 in the red, and 13 remained unchanged.

Flying Cement was the volume leader with 11.6 million shares traded, losing Rs0.10 to close at Rs0.16. It was followed by Pak Elektron with 8.14 million shares traded, gaining Rs0.18 to close at Rs2, and Ghani Global Holdings with 7.02 million shares traded, losing Rs0.64 to close at Rs14.68.

Business

An investigation was “launched” into PTA’s inability to get Rs. 78 billion back from Telcos

Rainfall throughout the night stops flights in Lahore.

Containers were used to seal the Red Zone before JI’s sit-in at D-Chowk.

Changes to Pakistan’s Test team could be significant for the Bangladesh series.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News3 days ago

Latest News3 days ago52 districts in Pakistan have 52 cases of the polio virus.

-

Latest News3 days ago

Latest News3 days agoFederal Cabinet once again postpones decision on PTI suspension and Article 6 action against Imran and Alvi

-

Entertainment3 days ago

Entertainment3 days agoA glimpse of Sania Mirza’s relaxed moments

-

Latest News3 days ago

Latest News3 days agoThe 10th Executive Committee Meeting of SIFC examines the role of provinces in bringing in foreign investment.

-

Latest News3 days ago

Latest News3 days agoCabinet will probably decide today whether to ban PTI: Fawad ChaudhryCabinet will probably decide today whether to ban PTI: Fawad Chaudhry

-

Latest News3 days ago

Latest News3 days agoElection Amendment Act Case Heard by IHC; Response Requested From Law Ministry, ECP Within Ten Days

-

Latest News3 days ago

Latest News3 days agoPakistan has advanced to the Women’s Asia Cup 2024 semifinals.

-

Latest News3 days ago

Latest News3 days agoMubarak Sani Case: Punjab Government’s Review Petition Accepted by the SC