Business

Rupee continues to strengthen against dollar as Dar takes charge of finance ministry

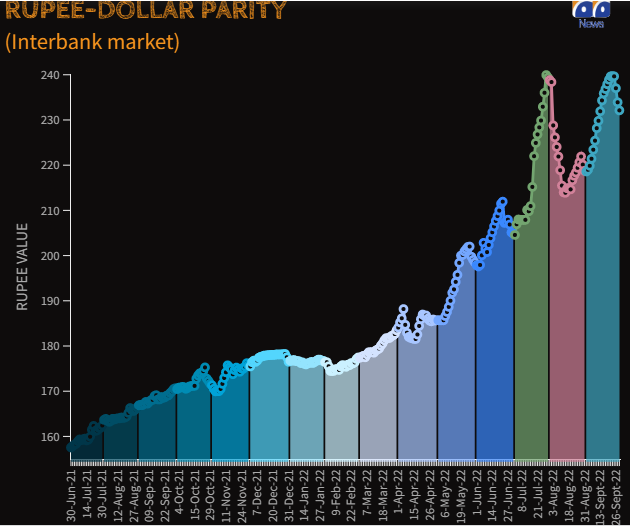

- Rupee continues gaining ground against dollar.

- Rupee gains 1.76, closes at 232.12 per dollar.

- Analysts cite return of Dar as reason behind increase.

KARACHI: The Pakistani rupee continued Wednesday to gain ground for the fourth consecutive session as the dollar’s slide persisted after federal minister Senator Ishaq Dar took charge of the finance ministry.

In the interbank market, the rupee gained 1.79 to close at 232.12 per dollar, according to the State Bank of Pakistan (SBP) after it increased its value by 7.53 in the ongoing week.

Currency dealers and analysts have cited that the return of Dar — a close aide of PML-N supremo Nawaz Sharif — to Pakistan to take charge as the finance minister has helped improve sentiment and the fall in international commodity prices boosted the rupee’s rise.

The current account deficit — fortunately — will likely remain in check on account of declining international commodity prices and administrative measures taken by the government.

Inflation, too, has most likely peaked and is expected to come down over the coming months, The News reported.

Talking to Geo.tv, economist and former adviser to the federal ministry of finance Dr Khaqan Hassan Najeeb said the first aspect is a change in market sentiment driven by a leadership change at the finance ministry.

“The new team is regarded to be more conscious of rupee movement and thus leaning to more orderly movement,” the former adviser said.

Secondly, he noted that some fundamentals have improved, especially a decline in oil prices as well as other key commodity prices, which may help reduce the quantum of imports.

“Thirdly, the confirmation by multilateral lenders to extend flood support is a market supporting development,” Dr Najeeb said.

Lastly, a bit farfetched but the possibility of reconsideration and leniency in some conditions by the International Monetary Fund (IMF) due to flood impact is driving a positive sentiment toward the rupee, Najeeb added.

Alfalah’s head of research Fahad Irfan said Dar would not have the kind of free hand he had in his previous term.

“The IMF, in general, has been much stricter in terms of policy implementation. Most importantly, Pakistan now has a free exchange rate regime, even otherwise, the country has record low forex reserves with no room to burn them to control the exchange rate,” he said.

“However, administrative curbs and stronger checks on manipulation and the smuggling of dollars out of Pakistan are still possible,” Irfan added.

He said the rupee was expected to regain some lost ground. However, with the fear of Dar, the pace of appreciation has accelerated.

He noted that changes in key positions, at times of catastrophic floods and an extremely fragile economic environment, might help Dar regain some lost popularity; however, this might slow down policymaking.

Dar maintained the rupee at a parity of 100 per dollar for his entire term (2013-2017) and kept the policy rate at its historic low of 5.75% from May 2016 to December 2017.

This lethal combo was the main reason why Pakistan posted a historic high current account deficit of $19.2 billion or 6.3% of the gross domestic product in FY2018 and eroded foreign exchange reserves to just 2 months of import cover, according to Irfan.

Dar seeks ‘time’ to stabilise Pakistan’s economy

Senator Dar has defended former finance minister Miftah Ismail’s policies as he sought time to stabilise Pakistan’s economy.

In a press conference outside an accountability court, Dar said Miftah is part of the government’s team and his efforts helped save the country from a looming default threat.

“Miftah put in all his efforts and through them, he saved Pakistan from default. The mess that was made in the last three to four years could not be cleared in four months,” he said.

Miftah had to take unpopular decisions, including raising power tariffs and rates of petroleum products, to restart the stalled International Monetary Fund (IMF) programme.

The belt-tightening measures invited criticism from the coalition rulers and Miftah received flak from his party as well.

In a separate conversation with journalists upon his arrival Dar said that he needed time to fix Pakistan’s economy.

Business

An investigation was “launched” into PTA’s inability to get Rs. 78 billion back from Telcos

Rainfall throughout the night stops flights in Lahore.

Containers were used to seal the Red Zone before JI’s sit-in at D-Chowk.

Changes to Pakistan’s Test team could be significant for the Bangladesh series.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News3 days ago

Latest News3 days ago52 districts in Pakistan have 52 cases of the polio virus.

-

Latest News3 days ago

Latest News3 days agoFederal Cabinet once again postpones decision on PTI suspension and Article 6 action against Imran and Alvi

-

Entertainment3 days ago

Entertainment3 days agoA glimpse of Sania Mirza’s relaxed moments

-

Latest News3 days ago

Latest News3 days agoThe 10th Executive Committee Meeting of SIFC examines the role of provinces in bringing in foreign investment.

-

Latest News3 days ago

Latest News3 days agoCabinet will probably decide today whether to ban PTI: Fawad ChaudhryCabinet will probably decide today whether to ban PTI: Fawad Chaudhry

-

Latest News3 days ago

Latest News3 days agoElection Amendment Act Case Heard by IHC; Response Requested From Law Ministry, ECP Within Ten Days

-

Latest News3 days ago

Latest News3 days agoPakistan has advanced to the Women’s Asia Cup 2024 semifinals.

-

Latest News3 days ago

Latest News3 days agoMubarak Sani Case: Punjab Government’s Review Petition Accepted by the SC