Business

PSX weekly review: KSE-100 posts highest weekly gain since July 2020

- Investors cheer decline in international oil and coal prices, which fuelled a rally at the bourse.

- KSE-100 index jump 3.7% — the highest weekly return since July 31, 2020.

- The market witnessed an eventful week owing to political, economic developments.

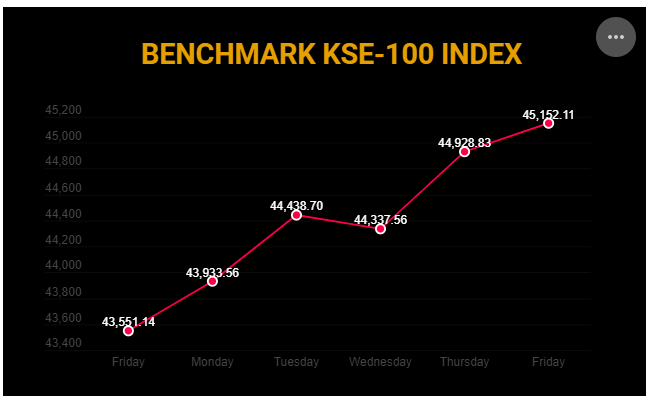

KARACHI: The bulls maintained their dominancy at the Pakistan Stock Exchange (PSX) as the KSE-100 index jumped 3.7% — the highest weekly return since July 31, 2020. The KSE-100 index posted gains of 1,601 points to settle at 45,152.11 points.

Investors cheered the decline in international oil and coal prices, which fuelled a rally at the bourse.

The market witnessed an eventful week as both, the incumbent PTI government and the Opposition tried to gather allies amid a vote of a no-confidence motion against Prime Minister Imran Khan in the National Assembly.

The market largely digested the aforementioned development, coupled with a decline in international oil and coal prices (which garnered interest in the cement sector) bringing back the bulls, as concerns over inflation ceded.

Although some shuffling in support by minority parties in the mid-week added pressure, the market witnessed a noteworthy jump of over 1,000 points.

Market players ignored all negative cues, including historic low rupee value against the US dollar, inconclusive talks with the International Monetary Fund (IMF), depleting foreign exchange reserves and rising inflation which jumped to 12.7% in March.

Other major developments during the week were: Lucky Cement unveiled a solar project, Economic Coordination Committee approved local gas supply to two urea plants, Oil and Gas Regulatory Authority (OGRA) took up issues relating to Price Differential Claims (PDC), international freight equalisation margin (IFEM) with stakeholders, Mari Petroleum Company commenced production at Sachal gas processing complex, banks and DFIs approved Rs435 billion loans under Temporary Economic Refinance Facility (TERF), revealed SBP governor, Asian Development Bank signed $300 million loan deal for Pakistan’s market development programme, and Ghandhara commenced booking for newly-launched SUVs.

Meanwhile, foreign selling continued this week, clocking in at $15.55 million against a net sell of $4.12 million recorded last week. Selling was witnessed in commercial banks ($13.7 million), and fertiliser ($0.6 million).

On the domestic front, major buying was reported by banks/DFIs ($15.7 million), followed by individuals ($7.5 million).

During the week under review, average volumes clocked in at 310 million shares (up by 116% week-on-week), while average value trade settled at $44 million (up by 72% week-on-week).

Major gainers and losers of the week

Sector-wise positive contributions came from cement (+266 points), commercial banks (+241 points), technology and communication (+182 points), fertiliser (+152 points), and power generation and distribution (+111 points). On the flip side, negative contributions came from leather and tanneries (-9 points), and leasing companies (-1 point).

Scrip-wise major gainers were Systems Limited (+129 points), Lucky Cement (+129 points), Millat Tractors (+69 points), Hubco (+68 points) and Engro Corporation (+6 points). Meanwhile, major losers were Colgate-Palmolive (-16 points), Services Pakistan (-9 points), and Engro Fertiliser (-6 points).

Outlook for next week

A report from AHL predicted: “Political noise is expected to be pushed back after the vote of no-confidence against PM Imran Khan on Sunday.”

“Moreover, with Ukraine-Russia peace talks in progress, commodity prices are expected to further decline,” it said.

“The KSE-100 is currently trading at a PER of 4.9x (2022) compared to the Asia-Pacific regional average of 12.3x while offering a dividend yield of 8.4% versus 2.5% offered by the region,” the brokerage house stated.

Business

An investigation was “launched” into PTA’s inability to get Rs. 78 billion back from Telcos

Rainfall throughout the night stops flights in Lahore.

Containers were used to seal the Red Zone before JI’s sit-in at D-Chowk.

Changes to Pakistan’s Test team could be significant for the Bangladesh series.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News3 days ago

Latest News3 days ago52 districts in Pakistan have 52 cases of the polio virus.

-

Latest News3 days ago

Latest News3 days agoFederal Cabinet once again postpones decision on PTI suspension and Article 6 action against Imran and Alvi

-

Entertainment3 days ago

Entertainment3 days agoA glimpse of Sania Mirza’s relaxed moments

-

Latest News3 days ago

Latest News3 days agoElection Amendment Act Case Heard by IHC; Response Requested From Law Ministry, ECP Within Ten Days

-

Latest News3 days ago

Latest News3 days agoThe 10th Executive Committee Meeting of SIFC examines the role of provinces in bringing in foreign investment.

-

Latest News3 days ago

Latest News3 days agoCabinet will probably decide today whether to ban PTI: Fawad ChaudhryCabinet will probably decide today whether to ban PTI: Fawad Chaudhry

-

Latest News3 days ago

Latest News3 days agoMubarak Sani Case: Punjab Government’s Review Petition Accepted by the SC

-

Latest News3 days ago

Latest News3 days agoPakistan has advanced to the Women’s Asia Cup 2024 semifinals.