Business

Lacklustre week drags PSX downward

- Investors remained on the sidelines in outgoing week.

- Moody’s decision, rupee-dollar party played on investors’ minds.

- KSE-100 index declined 137 points or 0.3%.

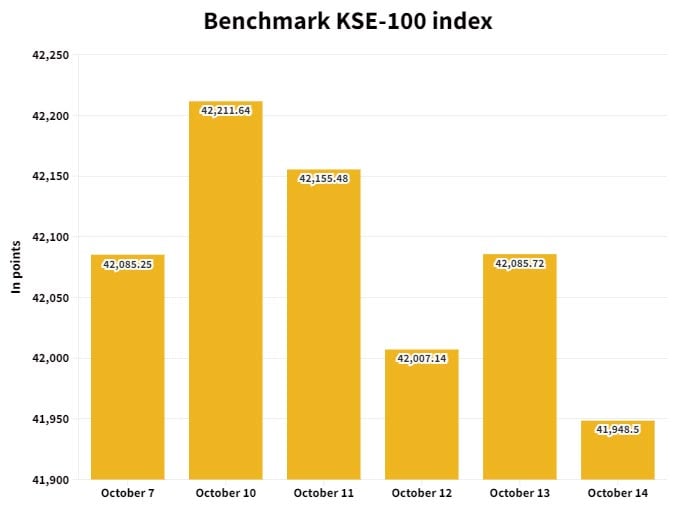

KARACHI: The Pakistan Stock Exchange (PSX) witnessed tepid trading in the outgoing week as Moody’s rating kept market participants mostly on the sidelines.

Moody’s decision, fluctuating rupee-dollar parity, and dwindling foreign exchange reserves played on investors’ minds during the week. Resultantly, the KSE-100 index declined 137 points or 0.3% to end the week at 41,948.50 points.

The market commenced the week on a positive note as investors’ interest revived on optimism that the State Bank of Pakistan (SBP) would maintain a status quo in its monetary policy announcement.

Investors’ interest was also fuelled by a statement from Finance Minister Ishaq Dar that Pakistan would not seek debt restructuring from the Paris Club and would meet all multi-lateral and international payment obligations.

The stock market, however, reversed the trend on Tuesday as investors opted for profit-booking owing to political and economic uncertainty.

The market extended losses as selling pressure continued to dominate as investors remained concerned over Moody’s downgrading five of Pakistan’s major banks. Investors took a cautious stance and resorted to value buying which led to some recovery during Wednesday’s session.

The bourse bounced back on Thursday and cushioned the dip amid renewed interest in selected stocks of the technology sector.

The index reversed its direction once again on the last trading session as a lack of positive triggers kept market players away from healthy participation, providing bears with an opportunity to dominate most of the trading session.

Other major developments during the week were: PSO wins arbitration case against Gunvor over LNG payments, Securities and Exchange Commission of Pakistan (SECP) registered 2,434 new firms in September, gas condensate discovered in Sanghar, inflation rate at 19.9%, IMF projected 3.5% growth for 2023.

Meanwhile, foreign buying continued this week, clocking in at $12.3 million against a net buy of $4.7 million recorded last week. Buying was witnessed in technology ($12.4 million), power (0.8 million), and cement ($0.3 million).

On the domestic front, major selling was reported by broker proprietary trading ($4.8 million), followed by companies’ finance institutions ($4 million).

During the week under review, average volumes clocked in at 267 million shares (down by 39% week-on-week), while the average value traded settled at $44 million (down by 7% week-on-week).

Major gainers and losers of the week

Sector-wise negative contributions came from technology and communication (-117 points), commercial banks (-48 points), tobacco (-32 points), cement (-15 points), and engineering (-12 points)

On the flip side, positive contributions came from exploration and production (+46 points) and refinery (+22 points)

Scrip-wise major losers were TRG Pakistan (-207 points), Pakistan Tobacco Company (-32 points), Meezan Bank (-24 points), Engro Fertiliser (-19 points), and Engro Corporation (-18 points).

Meanwhile, gainers were Systems Limited (+83 points), Pakistan Oilfields (+20 points), Lotte Chemical (+17 points), Oil and Gas Development Company (+16 points), and Nestle Pakistan (+15 points).

Outlook for next week

A report from Arif Habib Limited stated that the market is expected to remain positive in the upcoming week,” given the anticipation of FATF decision over the expected exit of Pakistan from the grey list.”

“Moreover, with the ongoing result season, certain sectors and scrips are expected to stay under the limelight given the anticipation of robust results,” it said.

“The KSE-100 is currently trading at a PER of 4.1x (2023) compared to the Asia-Pacific regional average of 12x while offering a dividend yield of 9.8% versus 3% offered by the region,” the brokerage house stated.

Minutes after taking off from Lahore airport, a private airline plane was “hit by a bird.”

Deputy Prime Minister to Represent Pakistan at CHOGM in Samoa in 2024

China Contributes 43 New Foreign Firms to the 6% Growth in SECP Registrations

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Snap launches tools for parents to monitor teens’ contacts

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Entertainment2 days ago

Entertainment2 days agoReham Khan’s counsel to Hania Amir between marriage versus career

-

Latest News1 day ago

Latest News1 day agoThe government and the military are successfully combating drug abuse through a nationwide anti-drug operation.

-

Latest News1 day ago

Latest News1 day agoAt a ceremony held at Mirpur, the Prime Minister of Jammu and Kashmir stated, “We will not hesitate to make any sacrifice for peace in the region.”

-

Latest News1 day ago

Latest News1 day agoThe 26th Amendment to the Constitution: The Amendment That Completes the Charter of Democracy: Bilawal

-

Latest News1 day ago

Latest News1 day agoIn the border region, a Lahore police officer was detained for allegedly using drones to smuggle drugs.

-

Entertainment2 days ago

Entertainment2 days agoThe Punjab government initiates the ‘Dhee Rani’ initiative for underprivileged couples.

-

Latest News1 day ago

Latest News1 day agoPakistan’s Deputy Prime Minister will be present at the Commonwealth Heads of Government Meeting, which will take place in Samoa.

-

Latest News1 day ago

Latest News1 day agoJudicial Appointments in the Supreme Court Will Be Made Transparent: Law Minister