Business

SBP-held reserves tick up by $18m

- Central bank did not mention any specific reason.

- Net forex reserves held by commercial banks stand at $5.5bn.

- Total liquid foreign reserves clock in at $9.8 billion.

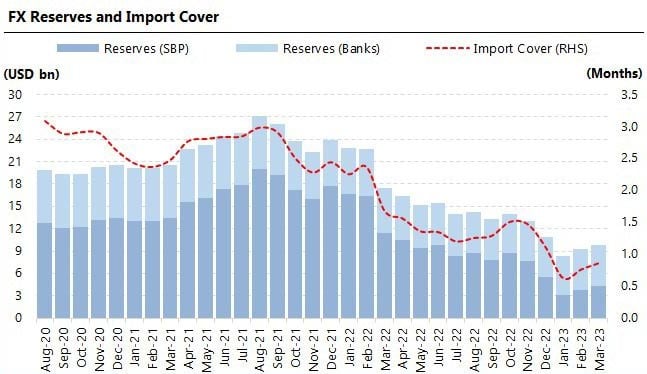

Pakistan’s foreign exchange reserves held by the State Bank of Pakistan (SBP) rose to $4,319 million in the week ending on March 10, the central bank said on Thursday.

Pakistan’s foreign exchange reserves held by the State Bank of Pakistan (SBP) rose to $4,319 million in the week ending on March 10, the central bank said on Thursday.

The central bank, in its weekly bulletin, said that its foreign exchange reserves have increased by $18 million to $4,319.1 million as of the week ended March 10, which will provide an import cover of around a month.

The net forex reserves held by commercial banks stand at $5,527.7 million, $1,208.6 billion more than the SBP, bringing the total liquid foreign reserves of the country to $9,846.8 million, the statement mentioned.

The central bank did not mention any specific reason behind an increase in SBP-held reserves.

Pakistan faces the renewed risk of recession amid a deepening political and economic crisis and a delay in the revival of the International Monetary Fund’s (IMF) bailout programme.

Bloomberg survey showed that the probability of the economy slipping into recession stands at 70%, according to the median forecast of 27 economists.

In the last few months, the cash-strapped nation has failed to meet several deadlines to secure funds to stave off a default, which has raised concerns that Pakistan might have to pause debt repayments.

In order to woo the IMF, Prime Minister Shehbaz Sharif-led government have raised taxes, cut energy subsidies, and hiked interest rates to a 25-year high to tamp down prices, but some issues are yet to be resolved.

Pakistan needs funds to revive its $350 billion economy, ease widespread shortages and rebuild its foreign currency reserves.

The nation’s dollar stockpile has fallen to less than a month’s worth of imports, restricting its ability to fund overseas purchases, stranding thousands of containers of supplies at ports, forcing plant shutdowns and putting tens of thousands of jobs at risk.

Lahore, PP-161: LHC deems the ECP recounting order null and invalid

The LHC has issued a summons regarding the policy on wheat procurement.

Lahore experiences a winter-like ambiance following rainfall.

Barwaan Khiladi: Kinza Hashmi discusses her role as Alia

Snap launches tools for parents to monitor teens’ contacts

Bannu Cantonment Board CEO Bilal Pasha ‘commits suicide’

Learn First | How to Create Amazon Seller Account in Pakistan – Step by Step

Sajjad Jani Funny Mushaira | Funny Poetry On Cars🚗 | Funny Videos | Sajjad Jani Official Team

Pakistan Reaction On Huge Win Against India | Pakistani Celebs Celebrate World T20 Cricket

-

Latest News2 days ago

Latest News2 days agoThree injured and two died in a Punjabi road accident

-

Latest News3 days ago

Latest News3 days agoIn KP rain-related incidents, ten people died.

-

Latest News3 days ago

Latest News3 days agoPM Shehbaz will meet with Saudi ministers and speak at the WEF special session today.

-

Latest News3 days ago

Latest News3 days agoPunjab takes action against factories that generate smoke.

-

Latest News3 days ago

Latest News3 days agoThe nomination of Ishaq Dar as deputy prime minister raises concerns.

-

Latest News3 days ago

Latest News3 days agoThe green colour of WhatsApp ‘angers’ some users.

-

Latest News3 days ago

Latest News3 days agoFarmers in Punjab file a lawsuit before the LHC, challenging the government’s unwillingness to purchase wheat.

-

Business3 days ago

Business3 days agoOver 500 points are lost by PSX stocks during intraday trading.