Business

Rupee registers handsome losses in pre-monetary policy session

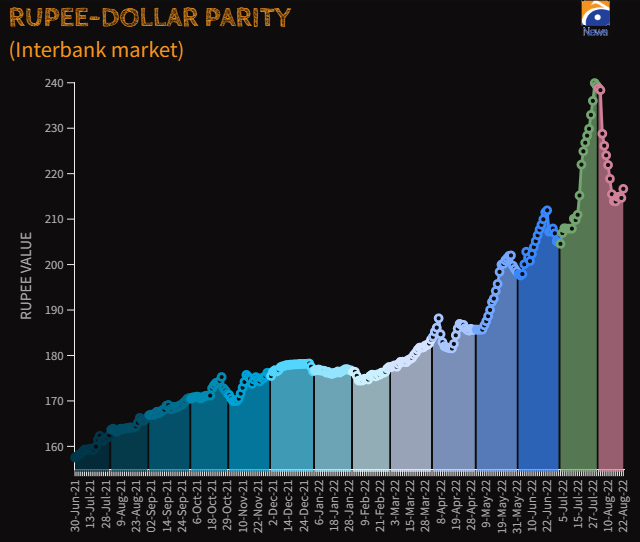

- In interbank market, rupee fell 2.01 or 0.93%.

- The local unit closes at 216.66 against dollar.

- Rupee fell 0.31% against greenback last week.

KARACHI: The Pakistan rupee lost ground against the US dollar Monday ahead of the monetary policy announcement — scheduled for today — and the speculations surrounding the International Monetary Fund (IMF).

In the interbank market, the rupee fell 2.01 or 0.93% against the dollar to close at 216.66, down from Friday’s close of 214.65, according to data from the State Bank of Pakistan (SBP).

The greenback traded at 213-214 during the outgoing week. It closed at 213.98 per dollar on Monday and finished at 214.65 on Friday. The rupee fell 0.31% against the greenback last week.

Economist and former adviser to the federal ministry of finance Dr Khaqan Hassan Najeeb said the local unit slipped by Rs2 against the dollar due to political developments and the strengthening of the dollar internationally.

“But we also know the economic situation remains challenging. SBP reserves are weak at $7.8 billion — hardly enough for over a month of imports,” he said.

Non-oil imports are curbed by SBP by rationing the opening of letter of credit (LC), the economist said, adding that oil is already in excess, so oil imports are low.

“Point being, we are operating in a restricted environment, and there would be import needs piling up.”

Getting flows including IMF money, multilateral and bilateral monies, and new foreign direct investment (FDI) is essential to normalise the balance of payments.

“Of-course exports drop and remittance slowdown in July must be looked at carefully.”

Talking to The News, a trader said that apart from forex inflows and outflows, the monetary policy decision will be instrumental to gauge the rupee’s future direction.

Another factor that weakened the rupee was a shortage of greenback in the open market, which moved up the rate of the interbank price of the dollar as well.

The government lifted a ban on the import of non-essential and luxury goods to meet a condition of the IMF ahead of the board’s meeting later this month to revive the loan programme.

However, it announced the imposition of heavy duties on completely built units cars, mobile phones, and electronic appliances to discourage imports.

The market will also evaluate the impact of opening up luxury imports on the rupee, according to traders.

The foreign currency reserves have started to recover. The foreign reserves held by the central bank slightly increased by $67 million or 0.9% to $7.9 billion as of August 12.